Total 365 Questions |

Updated On: Jun 15, 2026

Start Your Succesful IT Certification Journey With 3 Easy Steps!

1

DOWNLOAD PDF QUESTIONS

- Experience Complete Access to Practice Exam Questions

- Obtain Genuine Dumps PDF Questions

- Access a Free Questions Demo

- Receive Complimentary Updates for 90 Days

2

PRACTICE SESSIONS ONLINE

- Free IT Exam Practice Online

- Diverse Question Sets

- Convenient Browser-Based Test Platform

- Instant Access, No Installation Needed

3

SUCCESSFUL OUTCOME

- Efficient Exam Preparation

- Achieve High Grades

- Success Assured

- Kickstart a Brilliant Professional Career

Free CFA Institute CFA-Level-III Practice Exams Questions 2026 - TheExamsLabs

Start Preparation with the Latest and Real 100% Free CFA Level III CFA-Level-III Exam Dumps Questions Practice 2026

Page: 1

/ 73

Question 1

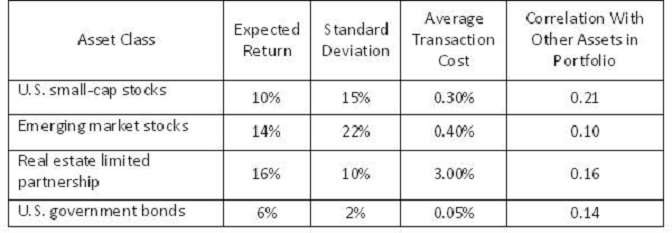

Dan Draper, CFA is a portfolio manager at Madison Securities. Draper is analyzing several portfolios whichhave just been assigned to him. In each case, there is a clear statement of portfolio objectives and constraints,as welt as an initial strategic asset allocation. However, Draper has found that all of the portfolios haveexperienced changes in asset values. As a result, the current allocations have drifted away from the initialallocation. Draper is considering various rebalancing strategies that would keep the portfolios in line with theirproposed asset allocation targets.Draper spoke to Peter Sterling, a colleague at Madison, about calendar rebalancing. During their conversation,Sterling made the following comments:Comment 1: Calendar rebalancing will be most efficient when the rebalancing frequency considers the volatilityof the asset classes in the portfolio.Comment 2: Calendar rebalancing on an annual basis will typically minimize market impact relative to morefrequent rebalancing.Draper believes that a percentage-of-portfolio rebalancing strategy will be preferable to calendar rebalancing,but he is uncertain as to how to set the corridor widths to trigger rebalancing for each asset class. As anexample, Draper is evaluating the Rogers Corp. pension plan, whose portfolio is described in Figure 1. Draper has been reviewing Madison files on four high net worth individuals, each of whom has a $1 millionportfolio. He hopes to gain insight as to appropriate rebalancing strategies for these clients. His research so farshows:Client A is 60 years old, and wants to be sure of having at least $800,000 upon his retirement. His risk tolerancedrops dramatically whenever his portfolio declines in value. He agrees with the Madison stock market outlook,which is for a long-term bull market with few reversals.Client B is 35 years old and wants to hold stocks regardless of the value of her portfolio. She also agrees withthe Madison stock market outlook.Client C is 40 years old, and her absolute risk tolerance varies proportionately with the value of her portfolio.She does not agree with the Madison stock market outlook, but expects a choppy stock market, marked bynumerous reversals, over the coming months.In selecting a rebalancing strategy for his clients, Draper would most likely select a constant mix strategy for:

Draper has been reviewing Madison files on four high net worth individuals, each of whom has a $1 millionportfolio. He hopes to gain insight as to appropriate rebalancing strategies for these clients. His research so farshows:Client A is 60 years old, and wants to be sure of having at least $800,000 upon his retirement. His risk tolerancedrops dramatically whenever his portfolio declines in value. He agrees with the Madison stock market outlook,which is for a long-term bull market with few reversals.Client B is 35 years old and wants to hold stocks regardless of the value of her portfolio. She also agrees withthe Madison stock market outlook.Client C is 40 years old, and her absolute risk tolerance varies proportionately with the value of her portfolio.She does not agree with the Madison stock market outlook, but expects a choppy stock market, marked bynumerous reversals, over the coming months.In selecting a rebalancing strategy for his clients, Draper would most likely select a constant mix strategy for:

Answer: C

Question 2

Carl Cramer is a recent hire at Derivatives Specialists Inc. (DSI), a small consulting firm that advises a varietyof institutions on the management of credit risk. Some of DSI's clients are very familiar with risk managementtechniques whereas others are not. Cramer has been assigned the task of creating a handbook on credit risk,its possible impact, and its management. His immediate supervisor, Christine McNally, will assist Cramer in thecreation of the handbook and will review it. Before she took a position at DSI, McNally advised banks and otherinstitutions on the use of value-at-risk (VAR) as well as credit-at-risk (CAR).Cramer's first task is to address the basic dimensions of credit risk. He states that the first dimension of creditrisk is the probability of an event that will cause a loss. The second dimension of credit risk is the amount lost,which is a function of the dollar amount recovered when a loss event occurs. Cramer recalls the considerabledifficulty he faced when transacting with Johnson Associates, a firm which defaulted on a contract with theGrich Company. Grich forced Johnson Associates into bankruptcy and Johnson Associates was declared indefault of all its agreements. Unfortunately, DSI then had to wait until the bankruptcy court decided on all claimsbefore it could settle the agreement with Johnson Associates.McNally mentions that Cramer should include a statement about the time dimension of credit risk. She statesthat the two primary time dimensions of credit risk are current and future. Current credit risk relates to thepossibility of default on current obligations, while future credit risk relates to potential default on futureobligations. If a borrower defaults and claims bankruptcy, a creditor can file claims representing the face valueof current obligations and the present value of future obligations. Cramer adds that combining current andpotential credit risk analysis provides the firm's total credit risk exposure and that current credit risk is usually areliable predictor of a borrower's potential credit risk.As DSI has clients with a variety of forward contracts, Cramer then addresses the credit risks associated withforward agreements. Cramer states that long forward contracts gain in value when the market price of theunderlying increases above the contract price. McNally encourages Cramer to include an example of credit riskand forward contracts in the handbook. She offers the following:A forward contract sold by Palmer Securities has six months until the delivery date and a contract price of 50.The underlying asset has no cash flows or storage costs and is currently priced at 50. In the contract, no fundswere exchanged upfront.Cramer also describes how a client firm of DSI can control the credit risks in their derivatives transactions. Hewrites that firms can make use of netting arrangements, create a special purpose vehicle, require collateralfrom counterparties, and require a mark-to-market provision. McNally adds that Cramer should include adiscussion of some newer forms of credit protection in his handbook. McNally thinks credit derivativesrepresent an opportunity for DSL She believes that one type of credit derivative that should figure prominently intheir handbook is total return swaps. She asserts that to purchase protection through a total return swap, theholder of a credit asset will agree to pass the total return on the asset to the protection seller (e.g., a swapdealer) in exchange for a single, fixed payment representing the discounted present value of expected cashflows from the asset.A DSI client, Weaver Trading, has a bond that they are concerned will increase in credit risk. Weaver would likeprotection against this event in the form of a payment if the bond's yield spread increases beyond LIBOR plus3%. Weaver Trading prefers a cash settlement.Later that week, Cramer and McNally visit a client's headquarters and discuss the potential hedge of a bondissued by Cuellar Motors. Cuellar manufactures and markets specialty luxury motorcycles. The client isconsidering hedging the bond using a credit spread forward, because he is concerned that a downturn in theeconomy could result in a default on the Cuellar bond. The client holds $2,000,000 in par of the Cuellar bondand the bond's coupons are paid annually. The bond's current spread over the U.S. Treasury rate is 2.5%. Thecharacteristics of the forward contract are shown below.Information on the Credit Spread Forward Determine whether the forward contracts sold by Palmer Securities have current and/or potential credit risk.

Determine whether the forward contracts sold by Palmer Securities have current and/or potential credit risk.

Answer: B

Question 3

Walter Skinner, CFA, manages a bond portfolio for Director Securities. The bond portfolio is part of a pensionplan trust set up to benefit retirees of Thomas Steel Inc. As part of the investment policy governing the plan andthe bond portfolio, no foreign securities are to be held in the portfolio at any time and no bonds with a creditrating below investment grade are allowable for the bond portfolio. In addition, the bond portfolio must remainunleveraged. The bond portfolio is currently valued at $800 million and has a duration of 6.50. Skinner believesthat interest rates are going to increase, so he wants to lower his portfolio's duration to 4.50. He has decided toachieve the reduction in duration by using swap contracts. He has two possible swaps to choose from:1. Swap A: 4-year swap with quarterly payments.2. Swap B: 5-year swap with semiannual payments.Skinner plans to be the fixed-rate payer in the swap, receiving a floating-rate payment in exchange. Foranalysis, Skinner always assumes the duration of a fixed rate bond is 75% of its term to maturity.Several years ago, Skinner decided to circumvent the policy restrictions on foreign securities by purchasing adual currency bond issued by an American holding company with significant operations in Japan. The bondmakes semiannual fixed interest payments in Japanese yen but will make the final principal payment in U.S.dollars five years from now. Skinner originally purchased the bond to take advantage of the strengtheningrelative position of the yen. The result was an above average return for the bond portfolio for several years.Now, however, he is concerned that the yen is going to begin a weakening trend, as he expects inflation in theJapanese economy to accelerate over the next few years. Knowing Skinner's situation, one of his colleagues,Bill Michaels, suggests the following strategy:"You need to offset your exposure to the Japanese yen by establishing a short position in a synthetic dualcurrency bond that matches the terms of the dual currency bond you purchased for the Thomas Steel bondportfolio. As part of the strategy, you will have to enter into a currency swap as the fixed-rate yen payer. Theswap will neutralize the dual-currency bond position but will unfortunately increase the credit risk exposure ofthe portfolio."Skinner has also spoken to Orval Mann, the senior economist with Director Securities, about his expectationsfor the bond portfolio. Mann has also provided some advice to Skinner in the following comment:"1 know you expect a general increase in interest rates, but I disagree with your assessment of the interest rateshift. I believe interest rates are going to decrease. Therefore, you will want to synthetically remove the callfeatures of any callable bonds in your portfolio by purchasing a payer interest rate swaption."After his lung conversation with Director Securities' senior economist, Orval Mann, Skinner has completelychanged his outlook on interest rates and has decided to extend the duration of his portfolio. The mostappropriate strategy to accomplish this objective using swaps would be to enter into a swap to pay:

Answer: B

Question 4

Albert Wulf, CFA, is a portfolio manager with Upsala Asset Management, a regional financial services firm thathandles investments for small businesses in Northern Germany. For the most part, Wulf has been handlinglocally concentrated investments in European securities. Due to a lack of expertise in currency management heworks closely with James Bauer, a foreign exchange expert who manages international exposure in some ofUpsala's portfolios. Both individuals are committed to managing portfolio assets within the guidelines of clientinvestment policy statements.To achieve global diversification, Wulf's portfolio invests in securities from developed nations including theUnited States, Japan, and Great Britain. Due to recent currency market turmoil, translation risk has become ahuge concern for Upsala's managers. The U.S. dollar has recently plummeted relative to the euro, while theJapanese yen and British pound have appreciated slightly relative to the euro. Wulf and Bauer meet to discusshedging strategies that will hopefully mitigate some of the concerns regarding future currency fluctuations.Wulf currently has a $1,000,000 investment in a U.S. oil and gas corporation. This position was taken with theexpectation that demand for oil in the U.S. would increase sharply over the short-run. Wulf plans to exit thisposition 125 days from today. In order to hedge the currency exposure to the U.S. dollar, Bauer enters into a90-day U.S. dollar futures contract, expiring in September. Bauer comments to Wulf that this futures contractguarantees that the portfolio will not take any unjustified risk in the volatile dollar.Wulf recently started investing in securities from Japan. He has been particularly interested in the growth oftechnology firms in that country. Wulf decides to make an investment of ¥25,000,000 in a small technologyenterprise that is in need of start-up capital. The spot exchange rate for the Japanese yen at the time of theinvestment is ¥135/€. The expected spot rate in 90 days is ¥132/€. Given the expected appreciation of the yen,Bauer purchases put options that provide insurance against any deprecation of the euro. While delta-hedgingthis position, Bauer discovers that current at-the-money yen put options sell for €1 with a delta of -0.85. Hementions to Wulf that, in general, put options will provide a cheaper alternative to hedging than with futuressince put options are only exercised if the local currency depreciates.The exposure of Wulf’s portfolio to the British pound results from a 180-day pound-denominated investment of£5,000,000. The spot exchange rate for the British pound is £0.78/€. The value of the investment is expected toincrease to £5,100,000 at the end of the 180 day period. Bauer informs Wulf that due to the minimal expectedexchange rate movement, it would be in the best interest of their clients, from a cost-benefit standpoint, tohedge only the principal of this investment.Before entering into currency futures and options contracts, Wulf and Bauer discuss the possibility of alsohedging market risk due to changes in the value of the assets. Bauer suggests that in order to hedge against apossible loss in the value of an asset Wulf should short a given foreign market index. Wulf is interested inexecuting index hedging strategies that are perfectly correlated with foreign investments. Bauer, however,cautions Wulf regarding the increase in trading costs that would result from these additional hedging activities.Regarding the Japanese investment in the technology company, determine the appropriate transaction in putoptions to adjust the current delta hedge, given that the delta changes to -0.92. Assume that each yen putallows the right to self ¥1,000,000.

Answer: A

Question 5

Geneva Management (GenM) selects long-only and long-short portfolio managers to develop asset allocationrecommendations for their institutional clients.GenM Advisor Marcus Reinhart recently examined the holdings of one of GenM's long-only portfolios activelymanaged by Jamison Kiley. Reinhart compiled the holdings for two consecutive non-overlapping five yearperiods. The Morningstar Style Boxes for the two periods for Kiley's portfolio are provided in Exhibits 1 and 2.Exhibit 1: Morningstar Style Box: Long-Only Manager for Five-Year Period 1 Exhibit 2: Morningstar Style Box: Long-Only Manager for Five-Year Period 2

Exhibit 2: Morningstar Style Box: Long-Only Manager for Five-Year Period 2 Reinhart contends that the holdings-based analysis might be flawed because Kiley's portfolio holdings areknown only at the end of each quarter. Portfolio holdings at the end of the reporting period might misrepresentthe portfolio's average composition. To compliment his holdings-based analysis, Reinhart also conducts areturns-based style analysis on Kiley's portfolio. Reinhart selects four benchmarks:1. SCV: a small-cap value index.2. SCG: a small-cap growth index.3. LCV: a large-cap value index.4. LCG: a large-cap growth index.Using the benchmarks, Reinhart obtains the following regression results:Period 1: Rp = 0.02 + H0.01(SCV) + 0.02(SCG) + 0.36(LCV) + 0.61(LCG)Period 2: Rp = 0.02 + 0.01(SCV) + 0.02(SCG) + 0.60(LCV) + 0.38(LCG)Kiley's long-only portfolio is benchmarked against the S&P 500 Index. The Index's current sector allocations areshown in Exhibit 3.Exhibit 3: S&P 500 Index Sector Allocations

Reinhart contends that the holdings-based analysis might be flawed because Kiley's portfolio holdings areknown only at the end of each quarter. Portfolio holdings at the end of the reporting period might misrepresentthe portfolio's average composition. To compliment his holdings-based analysis, Reinhart also conducts areturns-based style analysis on Kiley's portfolio. Reinhart selects four benchmarks:1. SCV: a small-cap value index.2. SCG: a small-cap growth index.3. LCV: a large-cap value index.4. LCG: a large-cap growth index.Using the benchmarks, Reinhart obtains the following regression results:Period 1: Rp = 0.02 + H0.01(SCV) + 0.02(SCG) + 0.36(LCV) + 0.61(LCG)Period 2: Rp = 0.02 + 0.01(SCV) + 0.02(SCG) + 0.60(LCV) + 0.38(LCG)Kiley's long-only portfolio is benchmarked against the S&P 500 Index. The Index's current sector allocations areshown in Exhibit 3.Exhibit 3: S&P 500 Index Sector Allocations GenM strives to select managers whose correlation between forecast alphas and realized alphas has beenfairly high, and to allocate funds across managers in order to achieve alpha and beta separation. GenM givesReinhart a mandate to pursue a core-satellite strategy with a small number of satellites each focusing on arelatively few number of securities.In response to the core-satellite mandate, Reinhart explains that a Completeness Fund approach offers twoadvantages:Advantage 1: The Completeness Fund approach is designed to capture the stock selecting ability of the activemanager, while matching the overall portfolio's risk to its benchmark.Advantage 2: The Completeness Fund approach allows the Fund to fully capture the value added from activemanagers by eliminating misfit risk.Which one of the following statements about Kiley's long-only portfolio is most correct1? Kiley's portfolio:

GenM strives to select managers whose correlation between forecast alphas and realized alphas has beenfairly high, and to allocate funds across managers in order to achieve alpha and beta separation. GenM givesReinhart a mandate to pursue a core-satellite strategy with a small number of satellites each focusing on arelatively few number of securities.In response to the core-satellite mandate, Reinhart explains that a Completeness Fund approach offers twoadvantages:Advantage 1: The Completeness Fund approach is designed to capture the stock selecting ability of the activemanager, while matching the overall portfolio's risk to its benchmark.Advantage 2: The Completeness Fund approach allows the Fund to fully capture the value added from activemanagers by eliminating misfit risk.Which one of the following statements about Kiley's long-only portfolio is most correct1? Kiley's portfolio:

Answer: C

Page: 1

/ 73

Total 365 Questions |

Updated On: Jun 15, 2026

© Copyrights TheExamsLabs 2026. All Rights Reserved

We use cookies to ensure your best experience. So we hope you are happy to receive all cookies on the TheExamsLabs.